Table of contents

Editor's note:

You've cracked e-commerce in Kenya. From Nairobi's CBD to Kisumu, your logistics are smooth. Your local payment integration is flawless, and your sales are climbing. You're success story in Kenya.

But when you look at a map of Africa, you see the opportunity to expand, but frustrating, invisible barriers wall you off. The payment systems you rely on at home can’t help you expand across Africa. And you don’t want to risk your hard-earned profits because of the horror stories you’ve heard about receiving payments from other African countries.

That’s where a good cross-border payment gateway comes in.

In this blog post, we’ll show you how to solve the common challenges of expanding from Kenya to the rest of Africa using Kora’s robust pan-African payment gateway. We'll cover currency conversion headaches, customer payment preferences, technical integration options, and security concerns that keep you up at night.

Four ecommerce payment challenges Kenyan businesses face

Here are four common challenges Kenyan businesses face when expanding across Africa and how to solve them with Kora.

1. Currency exchange and compatibility problems

Margins are everything for e-commerce businesses. You shouldn’t lose them to high cross-border fees and currency conversions.

In most cases, businesses have to rely on cross-border payment platforms built for consumers to receive money. This is problematic because these platforms usually have high exchange rates and aren’t built to facilitate large-scale trade. For example, say a customer in Nigeria wants to pay for a product on your website. First, they must download a cross-border payment app, sign up, and complete a clunky Know Your Customer (KYC) process. Depending on how long this takes, you have to deal with the settlement times, which are usually not instant.

Thinking of opening a Nigerian bank account from Kenya? The paperwork can be a significant hurdle. Moving the money to Kenya is even more difficult. Other businesses try stablecoins, but not every customer can find their way around crypto payments.

But Kora makes it easy for you. If you have a website and have technical resources, you can integrate Kora’s checkout through APIs. This embeds the checkout page on your website so customers can pay you using their favourite payment method. A Nigerian customer would see the option to pay with bank transfers, cards or Pay with Bank. A Ghanaian customer would see the option to pay with MTN MoMo.

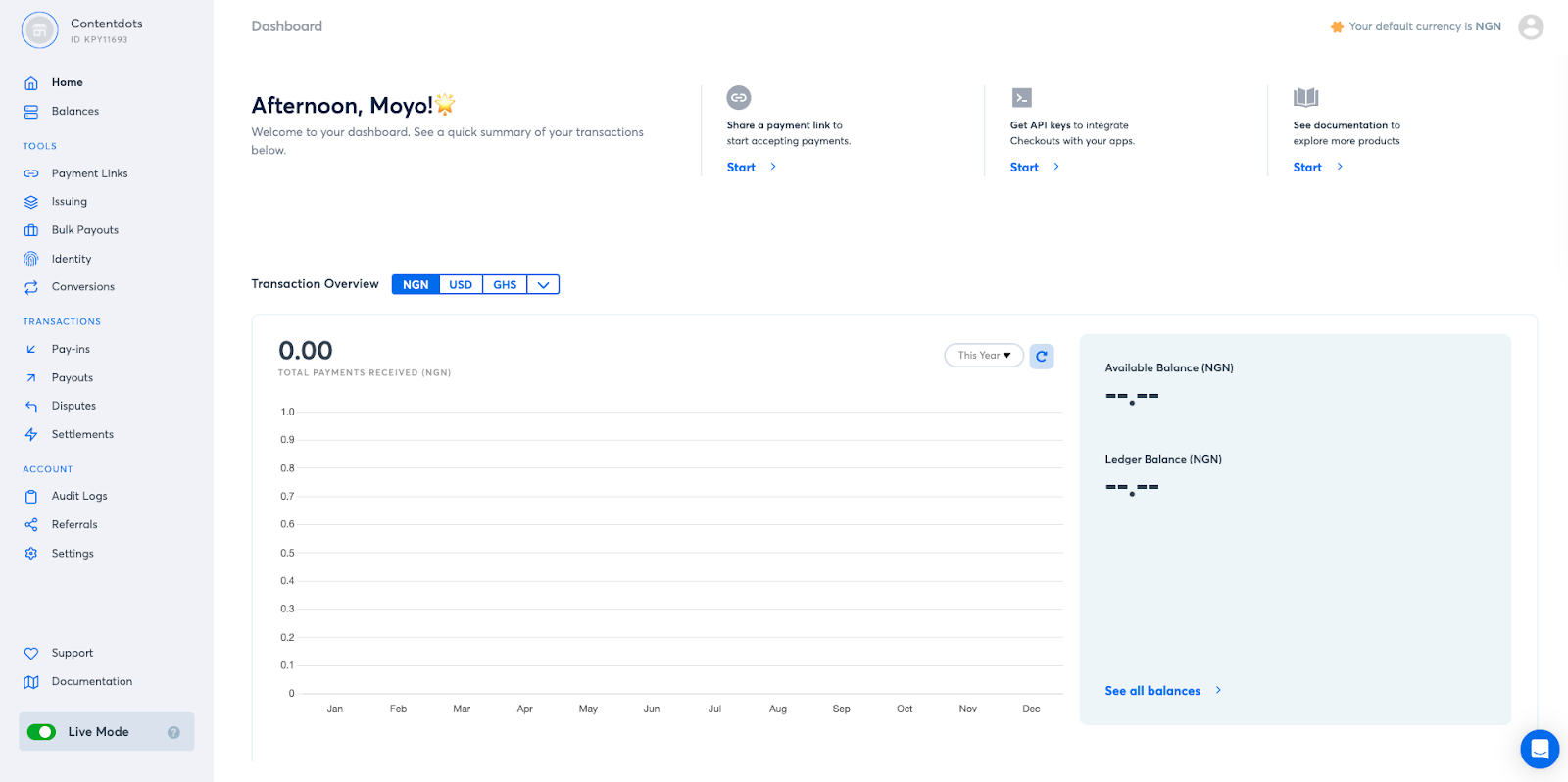

After you collect payments in Naira, on your dashboard, you can decide to settle in Kenyan Shillings. Kora has competitive conversion rates for businesses, so your fees won’t eat into your profit margin. Settlement is instant if customers pay you with bank transfers and Pay with Bank. For debit cards, settlement is T+1. If you want to swap these funds to Kenyan shillings, settlement is instant.

2. The customer experience gap: why African shoppers abandon carts

In Kenya, your checkout is seamless because customers know and trust M-Pesa or any other mobile money payment gateway you use. In other countries, you have to give them their preferred payment method or they’ll abandon their cart.

Most Ghanaian shoppers use MTN mobile money, as it owns 70% of Ghana’s telecom industry market share. A Nigerian customer prefers a direct bank transfer, and in South Africa, consumers prefer to use debit cards.

With Kora, you can bridge this trust gap by offering the exact local payment methods your customers in Ghana, Nigeria, and South Africa use every day, turning abandoned carts into completed sales.

Kora’s coverage:

- Nigeria: Bank transfers, Pay with Bank and Cards

- Ghana: Mobile Money (MTN Momo, Airtel Tigo, Vodafone)

- South Africa: Cards and EFT

- Cote d’Ivoire: Mobile Money (Vodafone, Orange, Etisalat)

- Cameroon: Mobile Money (MTN, Orange)

- Egypt: Mobile Money (MTN, Orange, Moov, Wave)

3. Payment failures and technical flexibility

Finding a payment gateway to scale across Africa is one thing, the other thing is finding one with the right payment tools specifically built for your business type and size.

If you sell on a website and are a small business, it may be difficult and expensive to hire and maintain an engineer to manage an integration for a payment gateway. That’s why we built Payment Links. They allow you to accept customer payments without spending money on technical resources. So, a Kenyan business that sells on Instagram, or any social media platform, can also use Kora to accept customer payments.

This is one of the tools Detail Africa uses to sell to customers in Ghana and Nigeria.

To create one, simply go to your Kora dashboard, click on “Payment Links”.

After, select your preferred currency and click “Create Payment Link”.

Then, fill in the necessary details and click “Create Payment Link” after.

After, copy the link and share it with your customers when they want to complete a purchase. You can use the same payment link once or multiple times, depending on your needs.

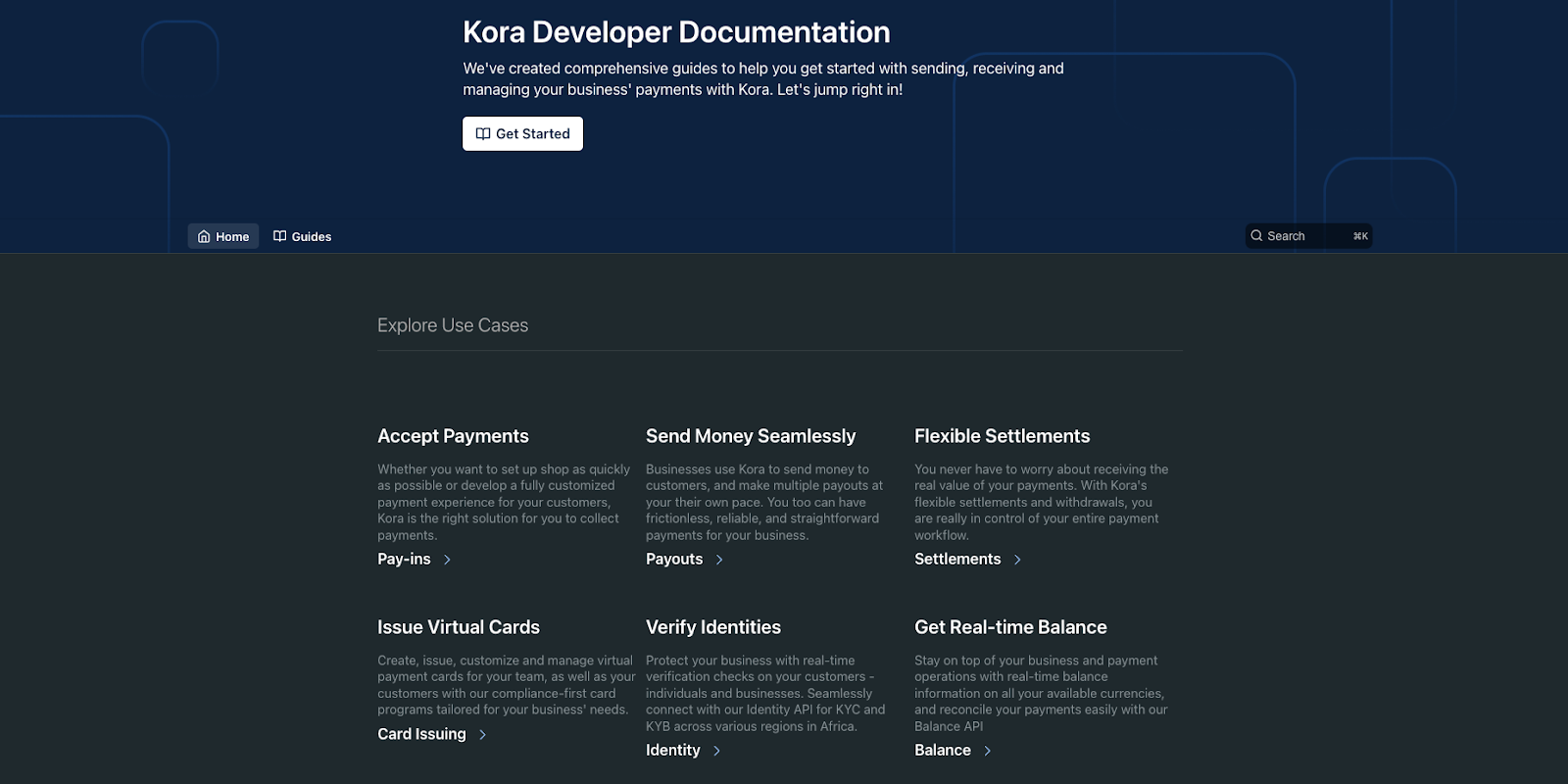

If you’re a large-scale e-commerce company with the right technical resources to integrate Kora into your website, explore our API docs here.

We pride ourselves on well-written and structured API docs that’ll make integration smooth as butter for your developers. They’re comprehensive, with clear code examples and search functionality.

4. Security and fraud prevention

You already face many security challenges when accepting payments in Kenya. Those challenges multiply when you start selling across Africa. That’s why your payment gateway needs to have solid security tools to protect you.

Robust Chargeback console

E-commerce businesses particularly face problems with chargeback fraud. In other cases, customers can also try to use stolen cards to purchase products in your store. Kora provides you with a robust chargeback console to manage chargebacks and prevent fraud.

Go to the Transactions section of the page and click on Disputes.

Then, click on the Chargebacks tab.

On the Chargebacks page, you see a list of pending chargebacks (along with their chargeback ID, customer name, date contested, due date, and chargeback amount).

Then click on the pending chargeback you want to address. To accept a chargeback, simply click Accept Chargeback, which means you have agreed to the customer’s claim.

To decline, click Decline. After that, you’ll be asked if it’s a partial or full decline, your reason for declining, and to upload the documents that validate your reason.

IP whitelisting

Hackers and fraudsters are always looking for ways to breach your bank account or the payment gateway you use. IP whitelisting helps to secure your Kora dashboard so that only you or anyone you grant permission to can access your dashboard.

This restricts access to only authorised IP addresses from your company. To enable this security feature, head to the Settings tab on your Kora dashboard.

Then select “Security”. After, click on the “Get Started” button beside the IP whitelisting option.

After, click on “Add IP Address” and you'll see a modal, then input the IP address you want to whitelist.

Afterwards, the dashboard will display a modal requiring you to input your 2FA code from your authentication app. Input the code, and that’ll enable the feature.

Then, click “Add IP Address” again, and you’ll see another modal asking you to input the IP you want to whitelist.

After inputting the IP, input the 2FA code from your authenticator app, and then you’ll be able to whitelist the IP address.

Remember, you can add as many as 20 IP addresses on your dashboard. There are other security tools on the Kora dashboard, like the 2FA authentication.

All these tools together help you protect your money from fraud, breaches, or loss.

Conclusion

Growing your e-commerce business from Kenya to across Africa can be smooth with the right payment gateway like Kora.

With Kora, you get access to tools that make accepting payments easy, competitive FX rates, and the right security tools to protect you from breaches.

.png)

%201.png)

%201.png)

%201.svg)

%201.png)

%201%20(1).png)